NZ ETS unit limits and price control settings for 2027–2031

Our 2026 advice on updating NZ ETS unit limits and price control settings for the next five years.

About this report

This report is the 2026 edition of our annual advice to the Minister of Climate Change on updating the New Zealand Emissions Trading Scheme unit limits and price control settings (NZ ETS settings), covering the years 2027–2031.

The Commission produces this advice as required by section 5ZOA of the Climate Change Response Act 2002 (the Act).

The Act was amended by the passing of the Climate Change Response (2050 Target and Other Matters) Amendment Bill in December 2025, altering some of the parameters for this advice. See Correspondence with the Minister of Climate Change below for further information.

Title: Advice on NZ ETS unit limits and price control settings for 2027–2031

Date: April 2026

ISSN: 3021-2669 (Online); 3021-2650 (Print)

Links

Download full report [PDF, 3.66 MB]

Media release:

Commission advises no change to NZ ETS settings but flags late-2020s risk

Technical and supporting documents

This technical annex provides further information on the data, methodology, and key assumptions we have taken to reach our final unit limit settings recommendations. This document should be read alongside Chapter 3: The NZ ETS emissions cap and Chapter 4: Unit limits in the main report.

Technical Annex 1: Unit limit settings [PDF, 1 MB]

Microsoft Word version [DOCX, 866 KB]

This technical annex provides further information on our analysis of the forestry emissions and removals included in the NZ ETS compared to target accounting, as calculated by the NZ ETS Forestry Model. It is used for the adjustment included in Step 1 of the unit limit settings method.

Technical Annex 2: Forestry accounting [PDF, 1.05 MB]

Microsoft Word version [DOCX, 1.10 MB]

This technical annex sets out in detail our assessment of how our recommendations comply with the accordance requirements in section 30GC of the Climate Change Response Act 2002, which stipulate that recommended NZ ETS settings are in accordance with emissions budgets and the 2050 target. It also contains a summary of how we have addressed other legislative requirements and matters.

Technical Annex 3: Assessment of Accordance [PDF, 417 KB]

Microsoft Word version [DOCX, 278 KB]

Supporting spreadsheet: 2026 NZ ETS settings advice

This supporting spreadsheet provides the data, analysis and calculations that informed our advice. It includes data for the charts and tables that appear in this report and in Technical Annex 1.

Spreadsheet: 2026 NZ ETS settings advice [XLSX, 1.10 MB]

NZ ETS Forestry model

This model projects allocations and surrenders of forestry NZUs since 2008 as well as emissions and removals by forests, based on data provided by the Ministry of Primary Industries and assumptions which can be varied. Within our analysis for NZ ETS settings advice, we have used this model to develop estimates of units held for post-1989 forest harvest liabilities, forestry emissions outside of the NZ ETS, and to determine the forestry technical adjustment in Step 1 of the unit limits method.

This model should be read in conjunction with the accompanying description document. Technical Annexes 1 and 2 discuss the assumptions applied.

Spreadsheet: NZ ETS Forestry Model [XLSX, 4.18 MB]

Description of NZ ETS Forestry Model [PDF, 215 KB]

Following the December 2025 amendments to the Act, the Commission and the Minister of Climate Change exchanged letters setting out the timing of the advice to the Minister, implications of recent legislative and policy developments, and some matters of interest to the Minister.

Downloads:

Commission's Letter to the Minister (18 December 2025) [PDF, 3.7 MB]

Minister's reply to the Commission (23 January 2026) [PDF, 300 KB]

Commission's Chair's reply to the Minister (30 January 2026) [PDF, 196 KB]

One page summary

A single-page overview of key points from this report.

One page summary [PDF, 1.02 MB]

FAQs

Questions and answers about this advice are available as a web page, or are available as a downloadable file. FAQS about this advice [PDF, 270 KB]

Executive summary

An executive summary is available below as a web page, or for download:

Background information

Explainer: What is the New Zealand Emissions Trading Scheme (NZ ETS)?

Executive summary

The information below is excerpted from the opening chapters of our full report. It is available below as a web page, or as a downloadable file:

Executive summary [PDF, 390 KB]

Microsoft Word version [DOCX, 314 KB]

About this report

This is our advice to the Government on unit limits and price control settings for the New Zealand Emissions Trading Scheme.

The New Zealand Emissions Trading Scheme (NZ ETS) is a key policy tool for reducing domestic greenhouse gas emissions. He Pou a Rangi Climate Change Commission provides the Government with regular advice on the scheme's unit limits and price control settings (NZ ETS settings). This is the fifth year the Commission has provided advice on NZ ETS settings. This advice covers the settings for 2027–2031.

After our recommendations were finalised, the current conflict began in the Middle East. The conflict has evolving implications for the supply and price of fossil fuels. Our advice already factors in uncertainty in the outlook for fossil fuel prices and Aotearoa New Zealand's emissions. The conflict has heightened that uncertainty, and could have further impacts across the economy, affecting emissions. Regular updates to NZ ETS settings allow the Government to keep the NZ ETS settings aligned with emissions targets while responding to uncertainty and changing circumstances. It will be important to reassess these issues in the next review of the NZ ETS settings, which under current legislation is scheduled for 2027 [i]

This advice is based on the Climate Change Response Act 2002 as it is currently in force. We also refer, where relevant, to the Government's announced intentions to amend this Act, shifting the next NZ ETS settings update to 2028. This reflects the information available to us about those plans at the time this advice was finalised.

Our recommendations

We are recommending that the Government maintain the current NZ ETS auction volumes through to 2030, and set 2031 auction volumes on the basis that the surplus of units in the market has been depleted by then. We are also recommending that the Government retain and extend to 2031 the current price control settings, with inflation adjustments from 2029.

Our recommendations balance two competing risks. On one hand it is possible that the current settings (or any reduction in volumes) will lead to an undersupply of units in the market later this decade. An undersupply could lead to rapidly rising and volatile New Zealand Unit (NZU) prices. This could unintentionally drive emissions reduction through plant closures and reduced production, rather than by incentivising investments in lower-emissions technologies.

On the other hand, a significant drop in NZU prices followed Government policy announcements on 4 November 2025. Market participants have reported that the perception of continued weakening of climate policy in general is contributing to low market sentiment. Any increase in auction volumes at this time to address the risk of undersupply could further undermine confidence in an already depressed market.

Our advice is therefore to maintain the current auction volume settings for now, while preparing to address the risk of a unit shortfall in future years.

Addressing the risk of a unit shortfall

We make our recommendations on the NZ ETS settings package on the basis that the next regulations update will be in 2027 as required by current legislation. On that basis, we advise the Government during the coming year to clearly signal and test with the market options for addressing the risk of undersupply in the years 2028–2030.

If the Climate Change Response Act 2002 is amended as the Government has announced it intends to, and the next settings update moves from 2027 to 2028, our advice would be for the Government to adopt a temporary lower tier of the cost containment reserve (CCR) [ii] to address the undersupply risk from 2028–2030.

We set out our recommendations in Table ES.1. Below we explain the key judgements, findings and areas of uncertainty that led us to this package of recommendations.

How we arrived at our recommendations

The Climate Change Response Act 2002 (the Act) requires that NZ ETS unit limits and price control settings accord with emissions budgets and the 2050 target. We aim to ensure accordance by using a method that is centred on this requirement and that also works through other matters that must be considered under the Act.

First, we assess how the country's emissions reduction goals can be shared across sectors inside and outside the NZ ETS, to give the emissions cap for the scheme. [iii] We then consider how much of that emissions cap is used up by units from industrial allocation [iv], overseas units, and surplus units already in the market. Any remaining volume under the emissions cap can be made available at auction. We also assess the emissions prices that could be needed to reduce emissions down to the emissions cap, to inform our judgements about the price control settings.

We consider that our recommended package of unit limits and price control settings strictly accords with the second emissions budget and the 2050 target. We also consider that the package accords with the third emissions budget, with a discrepancy that can be justified after considering relevant matters in the Act. This is set out in more detail in Chapter 5: Price control settings in this report and in Technical Annex 3: Assessment of accordance, published separately on our website.

NZ ETS emissions caps

We assess appropriate emissions caps to be 81.9 MtCO2e for the second (2026–30) and 28.9 MtCO2e for the third (2031–35) emissions budget periods.

These caps align with emissions budgets for those periods and are consistent with the Government's current emissions reduction plan. The emissions cap for the third emissions budget is based on an assumption that NZ ETS sectors will be responsible for closing all of the gap between currently projected emissions and the third emissions budget.

The emissions caps are lower than the Government announced when it decided on the last NZ ETS settings in August 2025. [v] More recent emissions projections show higher agricultural emissions, as well as greater CO2 removals by forests. As a result, those August 2025 caps no longer align with emissions budgets.

Our assessment of unit limits

We remove volume from the emissions cap to align with New Zealand's Greenhouse Gas Inventory

We assess that 4.3 MtCO2e should be subtracted from the emissions cap for the period 2027–31 to account for differences between the emissions reported under the NZ ETS and those estimated in New Zealand's Greenhouse Gas Inventory (GHG Inventory) [vi] and in target accounting. [vii]

Of these 'technical adjustments', 3.2 MtCO2e relates to forestry. A larger adjustment might be necessary depending on Government decisions on updating the NZ ETS default carbon yield tables. Those decisions are expected in 2026. If these yield tables are updated, our advice is that the Government should re-calculate and apply an updated value for the forestry-related technical adjustment.

The surplus of units in the market is continuing to decline

We estimate a surplus range from 17.1 to 41.7 million units, with a central estimate of 29.7 million units.

The surplus is depleting more quickly than previously expected, mainly because auctions have not cleared. Under current unit limit settings, the surplus was expected to reduce by 12.5 million units by the end of 2025. Our central surplus estimate has reduced by a further 6 million units because the 2025 auctions declined, and by another 1.9 million units due to updated data and assumptions.

Our estimated surplus range has also narrowed. This is mainly because the Ministry for Primary Industries (MPI) has provided us with updated data on forests, including estimates (by year of planting) of forests not likely to be harvested. This enabled us to calculate the surplus uncertainty associated with forests registered in the NZ ETS factoring in MPI's assumptions about their age.

Industrial allocation and overseas units

Our industrial allocation forecast is lower than in our 2025 advice, due to new data. [viii]

As in previous years, we recommend that the approved overseas unit limit be set at zero, as no overseas units have been approved for use in the NZ ETS.

Volume of units that could be made available at auction

The Government has adopted a goal of drawing down the surplus by 2030. Consistent with that goal, we estimate the volume that could be made available for auction over 2027–30 to be in a range from 11.2 million to 35.8 million units, with a central estimate of 23.2 million units. This compares to the auction volume under status quo settings of 11.7 million units for that period.

If status quo auction volumes are retained, there is a risk of a unit shortfall in the market towards the end of this decade. However, due to the current state of the market and the ability to reassess this risk in 2027, we are not recommending any changes to these auction volumes now. We explain these issues further below.

The risk of a unit shortfall

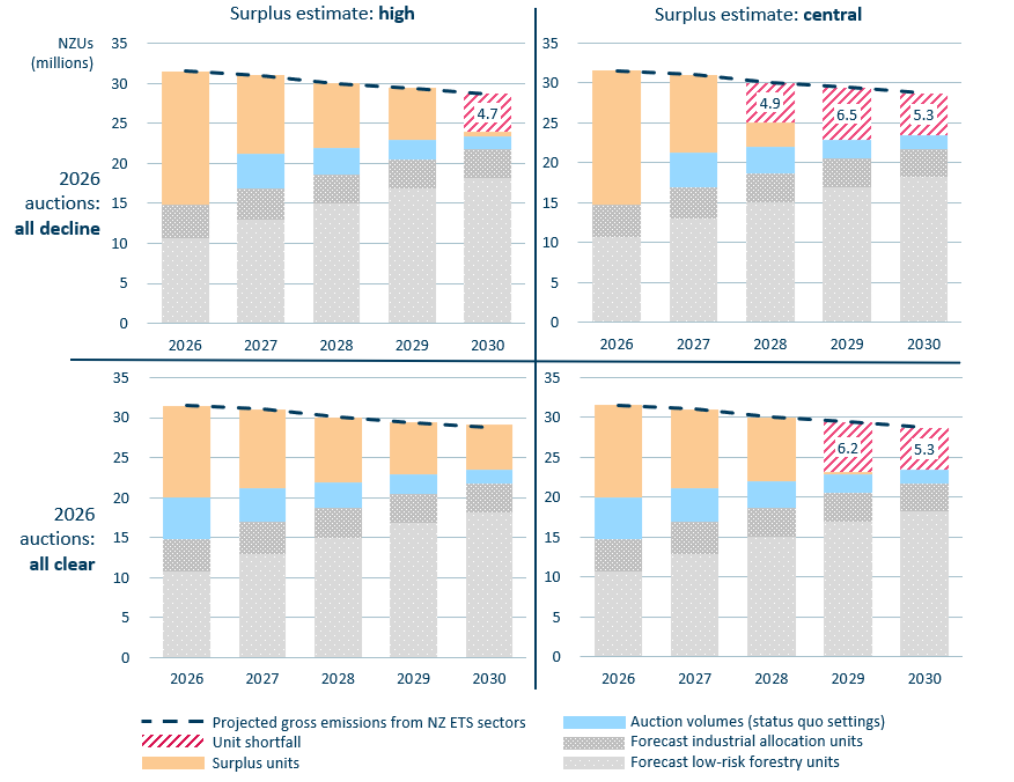

If the surplus is close to our central estimate, there is a risk that the market will be undersupplied later this decade. A unit shortfall could arise as early as 2028 if the surplus is close to our central estimate and the 2026 auctions do not clear. Even if the surplus is at the high end of our estimated range, there is a risk of undersupply if the 2026 auctions do not clear. As shown in Figure ES.1, the only scenario in which a shortfall does not occur is if the surplus is at the high end of the range and the auctions clear.

The surplus is dynamic, because market participants' behaviour can shift quickly as circumstances change. For example, we have heard that due to the recent drop and volatility in NZU prices, emitters have reduced their forward hedging so the surplus might currently be at the higher end of the range. But as the surplus depletes over time and the medium-term supply and demand fundamentals become clearer to the market, hedging practices could change, which could shift the surplus to lower levels closer to our central estimate.

The potential shortfall in 2028, based on our central estimate, could be around 5 million units. That is a significant volume in a market where annual demand from gross emissions totalled about 33 million units in 2025, and where the currently regulated auction volume for 2026 is 5.2 million units.

Whether and when this undersupply risk could materialise is uncertain. However, it is important that the Government consider how to mitigate this risk. If it does eventuate, its consequences could seriously undermine the effectiveness of the NZ ETS.

Potential impacts of a shortfall

Any shortfall could result in rapid increases and volatility in NZU prices. Rapid price changes have occurred before, such as in 2021–2022.

The emissions price in an ETS is intended to rise steadily over time to encourage emissions reductions. However, overly rapid price rises can outpace people's and businesses' ability to respond. Such price rises increase volatility, which undermines the scheme's ability to incentivise investments to reduce emissions, both in forestry and in other sectors. When returns are unpredictable, businesses are likely to delay investment decisions.

Volatile or rapidly rising NZU prices could also force emissions reductions through reduced production or plant closures (rather than incentivise investments in lower-emissions technologies), and create conditions where the Government is pressured to make ad hoc interventions in the market.

Figure ES.1: Scenarios demonstrating the risk of a unit shortfall from as early as 2028

Source: Commission analysis

Note: This figure shows two important dimensions of uncertainty, relating to the surplus and auctions. There is also uncertainty in the other elements of unit supply and demand shown in these charts, as they are projections.

Our recommended unit limits

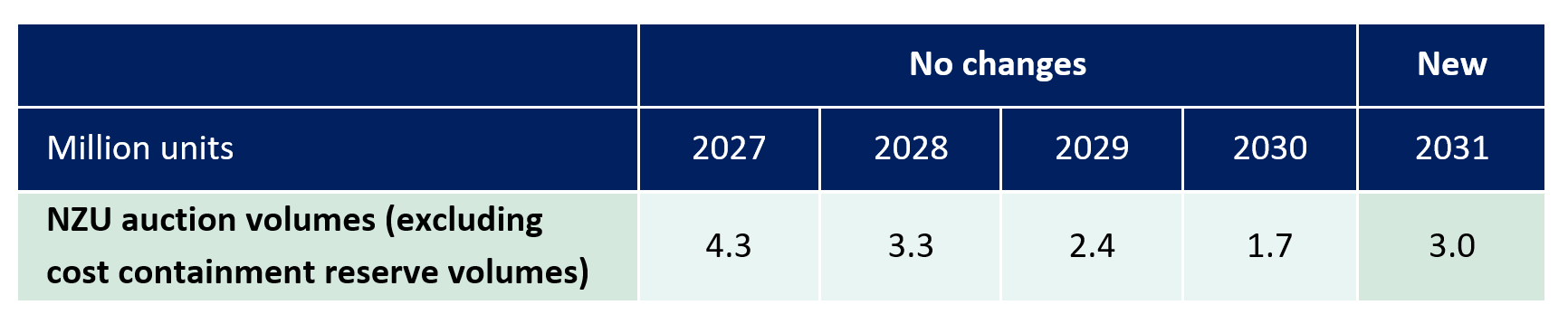

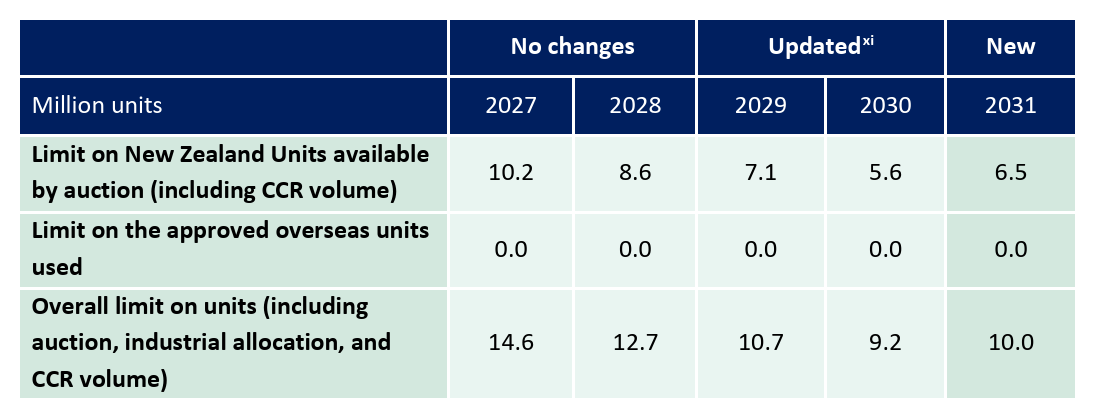

We are recommending that the Government maintain the current NZ ETS auction volumes through to 2030. We are also recommending that the Government set 2031 auction volumes on the basis that the surplus of units in the market has been depleted by that time. Table ES.1 shows our recommended unit limit settings.

Our recommendations are conditional on the next NZ ETS update going ahead in 2027

Our recommendation for the NZ ETS settings package is conditional on the next update of NZ ETS settings occurring in 2027 as currently required by the Act.

The Government has said it aims to support a stable and predictable NZ ETS market that provides incentives for investment in reducing emissions. To support that goal, market participants need clear signals about the likelihood of any future change to NZ ETS settings, including how the Government proposes to address the shortfall risk.

If the next update occurs in 2027 as the Act currently requires, we advise the Government to clearly signal and test with the market options for addressing undersupply risk that may need to be implemented over 2028–30 [ix]

What if the next NZ ETS update is not until 2028?

The Government has announced its intention to amend the Act so NZ ETS settings updates occur every two years instead of annually as at present. Depending on the timing of that amendment, the next NZ ETS settings update may not occur until late 2028. That would be too late for the Government update to address any risk of a shortfall that emerges during 2028.

If the proposed amendment goes ahead and there is no NZ ETS settings update in 2027, our advice would be to put in place now a temporary, lower tier of the cost containment reserve (CCR) for 2028–2030. The purpose of this new temporary CCR tier would be to mitigate the risk of a shortfall in 2028 that could lead to NZU prices rising too high, too fast.

The temporary CCR would have a trigger price above the current auction reserve price (ARP) [x] but below the current CCR and would only provide units to the market in the case of rapidly rising prices. It would contain the unit volumes that could be auctioned based on the central estimate of the surplus, but which we are otherwise recommending not be offered for auction in this year's settings update. These units, according to our best estimates, are within the NZ ETS emissions cap and could be auctioned without risking accordance with targets. If the next opportunity to update the settings is in 2028, this is the only option we have identified that can address undersupply risk in that year.

Why we are not recommending that those units be made available at auction

We have chosen not to recommend unit limits that would increase the base auction volume over the 2027–2030 period. This is primarily because of the current state of the market.

After several months of relatively stable prices in the $50–$60 range, the NZU spot price fell significantly in November 2025 and has been volatile since. The price reached the low $30s in January 2026 before climbing back into the $40s in early March. Auctions have declined because market participants can buy units on the secondary market at prices far below the current ARP.

We have not identified any reason based on the fundamentals of supply and demand for spot prices to be as low as they are. The price decline in November 2025 followed a series of Government decisions relevant to the NZ ETS. The Government in October 2025 announced a less ambitious 2050 target for reductions in biogenic methane. It also ruled out pricing of agricultural emissions. In November 2025 the Government then announced its intention to remove a requirement for NZ ETS settings to accord with Aotearoa New Zealand's nationally determined contributions (NDCs) under the Paris Agreement.

The agriculture announcements mean NZ ETS sectors such as forestry, transport and energy may need to do more if Aotearoa New Zealand is to meet its emissions budgets. The changes also create uncertainty for market participants, since the emissions reductions required of NZ ETS sectors may keep changing in response to trends in agricultural emissions.

The market participants we spoke with said the falling prices to a large extent reflected sentiment and uncertainty about climate policy. Those participants viewed recent NZ ETS and other climate policy announcements (relating to agriculture, transport and corporate climate reporting) as reflecting a general weakening in the Government's commitment to emissions reductions. They did not expect sentiment to improve or prices to recover enough during 2026 for auctions to clear.

They also said the price was weighed down by the short-term issue of increased units entering the market from forestry mandatory emissions returns due in the first six months of this year. Some indicated that increased forestry unit flows significantly contributed to the price lows experienced in January.

While additional volumes could be made available for auction in line with the Government's emissions budgets, our assessment is that offering those volumes under current circumstances might further undermine market confidence.

Why we are not recommending a further reduction in auction volumes

Some market commentators have suggested that reducing auction volumes in the years to 2030 could help the market recover from recent low and volatile prices. The Minister has also publicly expressed interest in whether reduced auction volumes in the short term might help the NZ ETS to deliver more emissions reductions and better position the Government to meet the emissions budgets and first NDC.

For the NZ ETS to effectively incentivise emissions reduction, emitters need to be able to make investment decisions based on clearly signalled information about future policies and settings. In our view, reducing auction volumes below current levels might not in itself encourage emitters to invest in decarbonisation. Instead, reducing auction volumes now could increase the risk of a unit shortfall, resulting in undesirably rapid and volatile price rises.

To get on track to meet the third emissions budget, additional policies complementary to the NZ ETS are likely to be necessary given what is known about the emissions reductions that are feasible over the period.

In our 2025 emissions reduction monitoring report, we examined the further potential to reduce emissions to meet the third emissions budget. Most opportunities identified were either not likely to respond to NZ ETS incentives (e.g. passenger vehicle mode shift and other opportunities in transport) or were in sectors not covered by the NZ ETS (e.g. agriculture), or in areas where the NZ ETS emissions price is unlikely to be consistently high or stable enough to drive change (e.g. electricity generation and industry).

Planting forests is the activity the NZ ETS is most likely to incentivise, and forests planted between now and 2031 can help with meeting the third emissions budget and second NDC (2031–2035), but not with meeting the first NDC (2021–2030). This is because new forests take 4–5 years after planting to start to sequester carbon. Withdrawing further units from auctions could encourage more afforestation, but those new forests would not provide units to the market to meet projected gross emissions demand in the years to 2030. Any further planting would not resolve the risk of a unit shortfall over 2028–2030.

Our recommended price control settings

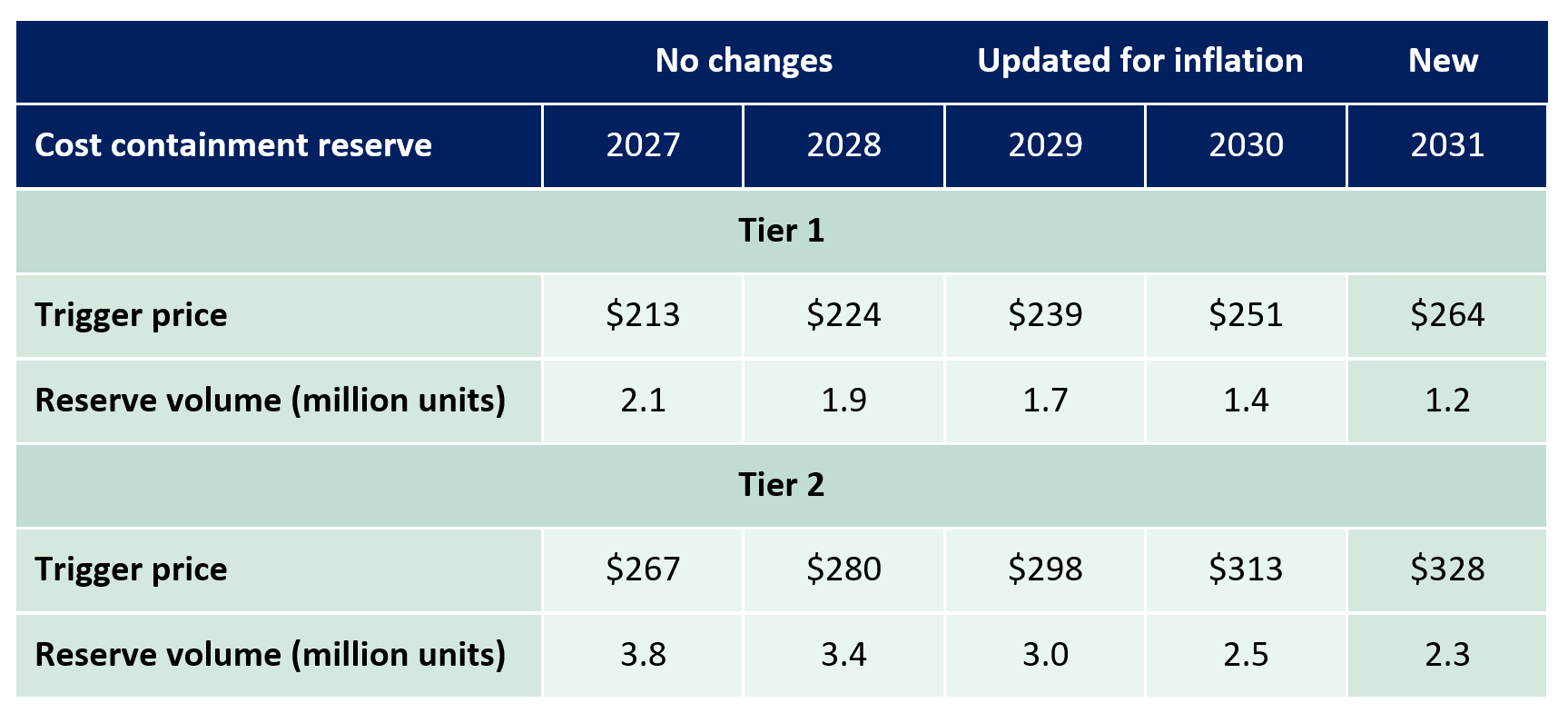

We are recommending that, for now, the ARP and CCR prices and volumes should remain at current levels and be extended on their current trajectory to 2031, with an inflation adjustment from 2029 onwards. These settings have remained consistent (aside from inflation adjustments) since 2022. Table ES.1 shows our recommended price control settings.

Why we are not recommending any increase in the ARP at this stage

We have considered whether raising the ARP would be beneficial in the short term. However, it is unclear that increasing the ARP would have any material effect on emissions in the short term. NZU spot prices are well below the current ARP. In the current context, market participants might perceive an increase in the ARP as an unexpected, confusing and unnecessary change, undermining any signal it might send about commitment to climate action.

In 2025 we advised that it may become necessary at some stage to increase the price levels of both the ARP and CCR, depending on the extent that gross emissions reductions are needed to meet the third emissions budget, and the likely cost of these. Both of these factors are very uncertain, as they will be affected by trends in fossil gas prices, EV uptake and afforestation. These uncertainties have not sufficiently resolved over the past year to justify any increase in the price control settings at this stage. We will monitor developments and address any necessary changes in future NZ ETS settings advice.

Why we are not recommending a lower ARP

The fact that NZU spot prices are currently below the ARP level does not provide any justification to lower it. Our analysis does not indicate that the minimum price needed to meet emissions budgets has reduced. Market participants have told us that current spot prices reflect sentiment change and are not connected to supply and demand fundamentals.

A lower ARP would be inconsistent with the known evidence about emissions prices needed to meet emissions budgets. It would undermine the Government's net-based approach to meeting emissions budgets (under which carbon removals by forests are intended to play an important role) by reducing incentives for afforestation. It could also increase the risk of the Government selling units below the cost of offshore mitigation, increasing the economic and fiscal costs of meeting the first and second NDC.

If afforestation between now and 2031 is sufficient to close the gap between current projections and the third emissions budget, there would be a case that the ARP no longer needed to increase after 2031 (except for inflation adjustments), but no case to lower the ARP as that would undermine forestry investments.

The NZ ETS’s contribution to emissions reduction

Globally, emissions pricing is an increasingly important tool for reducing greenhouse gas emissions. By 2025 there were 37 emissions trading schemes and 43 carbon taxes operating around the world. These schemes covered 28% of the world's greenhouse gas emissions (including China, the European Union and several of the largest states in the United States).

In Aotearoa New Zealand, the NZ ETS is well established and is playing a role in helping the country to meet its climate targets, particularly through encouraging afforestation. The Government has made it clear that it sees the NZ ETS as Aotearoa New Zealand's main tool for reducing emissions.

In December 2025 and January 2026 the Commission exchanged letters with the Minister of Climate Change discussing the context for this advice in light of recent statutory amendments. The Minister expressed interest in NZ ETS settings (including reducing auction volumes and a higher ARP) that would deliver additional emissions reductions towards meeting emissions budgets and NDC commitments. This report includes commentary on those areas.

Effective operation of the NZ ETS requires credible and well-signalled decisions about NZ ETS settings and climate policy more generally, in order to support investment in emissions reduction. As discussed above, our assessment is that short-term adjustments to the NZ ETS settings might further destabilise the market without bringing the reduction in emissions that the Government is seeking.

As advised in our 2025 emissions reduction monitoring report, our assessment is also that meeting emissions targets will require a strengthened NZ ETS together with additional targeted policies in areas such as renewable energy, transport and agriculture. The NZ ETS covers less than 40% of Aotearoa New Zealand's domestic net emissions, and in its current form is unlikely to drive significant emissions reduction in some of the sectors it does cover.

Our analysis suggests that from 2034 there may be no further volume to auction (as all gross emissions covered by the scheme will be covered by units from industrial allocation and forestry). The emissions cap, which is the key element of an ETS that enables it to incentivise reductions, could reduce to zero soon after. In addition, industrial allocation beyond that point is likely to allow emissions above the cap. There are factors that could shift this earlier, for example the revisions to emissions budgets due in 2027 or increases to projections of agricultural emissions.

In other words, the point is drawing closer at which the NZ ETS in its current form will no longer be able to incentivise further net emissions reductions, despite more reductions being needed to meet emissions budgets and the 2050 target.

To encourage the investments that will be needed to achieve further emissions reductions from 2034, the Government will need either to start now on a process to reform the structure and operation of the NZ ETS or implement a more comprehensive suite of other policies to reduce emissions, or both.

Our upcoming emissions monitoring report will provide further advice on progress towards emissions budgets and the 2050 target.

What happens next for NZ ETS settings?

This advice is one step within a wider process for updating the NZ ETS settings.

The Government will consider our advice and run a public consultation on proposals, which we understand will be led by the Ministry for the Environment on behalf of the Minister of Climate Change in the second quarter of 2026. The Government must make decisions on NZ ETS unit limits and price control settings in time for the regulations to be updated by 30 September 2026. The new settings will come into force on 1 January 2027.

Under current legislation we expect to provide our next advice on this topic, relating to the period 2028–2032, in early 2027.

Recommendations and proposed auction volumes

Proposed auction volumes

The tables below are image files and are not machine-readable. Download these tables as a spreadsheet (XLSX, 58 KB)

Recommended unit limits and price control settings

[xi] The overall limits for 2029 and 2030 have been updated to reflect an updated forecast of industrial allocation.

Footnotes

- The Climate Change Response Act 2002 (the Act) requires us to deliver our next advice on NZ ETS settings early in 2027. The Government has proposed to amend the Act to provide settings updates every two years. Information from the Ministry of the Environment on the proposed changes to the Act can be found here.

- The cost containment reserve (CCR) makes an additional volume of units available for sale if the price at government auctions exceeds a specified trigger price, to act as a brake on further price rises.

- Emissions budgets can be achieved through emissions reductions by sectors both inside and outside the NZ ETS. The NZ ETS emissions cap is the share of the emissions budget volume allocated to sectors in the NZ ETS. The emissions cap declines over time to reflect emissions reduction targets.

- ‘Industrial allocation’ (or ‘industrial free allocation’) is the provision of free NZUs to firms undertaking emissionsintensive-and-trade-exposed (EITE) activities. This reduces the cost of the NZ ETS for these firms and is intended to reduce the risk of emissions leakage.

- The Government announced an emissions cap of 89.4 MtCO2e for the second emissions budget (2026–30) and a 'provisional' cap of 40.7 MtCO2e for the third emissions budget (2031–35).

- New Zealand’s Greenhouse Gas (GHG) Inventory is the official annual report of all human-induced emissions and removals of greenhouse gases in Aotearoa New Zealand.

- Target accounting is the accounting system used to measure progress towards Aotearoa New Zealand’s emissions reduction goals. It includes all gross emissions as reported in the GHG Inventory, but only a subset of emissions and removals from land use and forestry.

- As industrial allocation is included in the overall limit on units, we have updated the overall limits from 2029 to reflect the revised forecast of industrial allocation. We have not updated the overall limits for first two years of the settings period (2027–2028) due to the Act’s restrictions on amending those years of the settings.

- Under the Act, the first two years of the settings period cannot be amended, except if certain circumstances arise such as a change significantly affecting a matter that must be considered under the Act. This is intended to support predictability.

- The auction reserve price (ARP) is the minimum price below which units will not be sold at government auctions.

- The overall limits for 2029 and 2030 have been updated to reflect an updated forecast of industrial allocation.

References

- Improving New Zealand’s climate change act. New Zealand Government; 2025.

- Honourable Simon Watts. Letter to CCC Chair regarding options for 2026 ETS settings advice. 2026. 23 January. https://www.climatecommission.govt.nz/assets/ETSadvice/2026/23-Jan-2026-Letter-to-CCC-Chair-regarding-options-for-2026-ETS-Settingsadvice.pdf

- He Pou a Rangi Climate Change Commission. Monitoring report: Emissions reduction. 2025. Annual Monitoring Report.

- World Bank Group. State and Trends of Carbon Pricing 2025. 2025.